taxman1

You are a resident, for U.S. federal tax purposes, if you are a Lawful Permanent Resident of the United States at any time during the calendar year. This is known as the "green card" test.

You are a Lawful Permanent Resident of the United States, at any time, if you have been given the privilege, according to the immigration laws, of residing permanently in the United States as an immigrant. You generally have this status if the U.S. Citizenship and Immigration Services (USCIS) issued you an alien registration card, Form I-551, also known as a "green card."

You continue to have U.S. resident status, under this test, unless:

If you meet the green card test at any time during the calendar year, but do not meet the substantial presence test for that year, your residency starting date is the first day on which you are present in the United States as a Lawful Permanent Resident. However, an alien who has been present in the United States at any time during a calendar year as a Lawful Permanent Resident may choose to be treated as a resident alien for the entire calendar year.

You will be considered a U.S. resident for tax purposes if you meet the substantial presence test for the calendar year. To meet this test, you must be physically present in the United States on at least:

1. 31 days during the current year, and

2. 183 days during the 3-year period that includes the current year and the 2 years immediately before that, counting:

You are treated as present in the United States on any day you are physically present in the country, at any time during the day. However, there are exceptions to this rule. For details on days excluded from the substantial presence test for other than exempt individuals, refer to Publication 519, US Tax Guide for Aliens.

An alien who meets either the green card or substantial presence test (described above) is considered a resident alien. However, there are exceptions to the substantial presence test for exempt individuals and for individuals with a “closer connection to a foreign country”.

For the substantial presence test, days of presence in the US do not count if an individual is temporarily present in the US as a:

Teacher or trainee under a “J” or “Q” visa (certain limits apply)

Filing requirements for exempt individuals. Generally, exempt individuals are considered nonresident aliens and file Form 1040NR. An individual who excludes days of presence under the definition of exempt individual must file Form 8843, Statement for Exempt Individuals and Individuals With A Medical Condition.

An alien is considered a nonresident alien unless either the green card or substantial presence (described above) test is met.

An individual can be both a resident alien and a nonresident alien during the same year. This dual status usually occurs in the year of arrival into or departure from the US. The taxpayer’s residency status on the last day of the year determines the form to be filed.

Resident files a tax return Form 1040 with “Dual-Status Return” across the top showing income from all sources for the residency portion of the year, plus US source income effectively connected with a trade or business from the non-residency portion of the year.

Nonresident taxpayer files a tax return Form 1040NR with “Dual-Status Return” across the top showing US-sourced income for the non-residency portion of the year, plus income from all sources for the residency port of the year.

For US citizens and resident aliens, a valid Social Security Number (SSN) must be used. Persons who require an SSN must file form SS-5 with IRS to obtain a number. (Please note that applicants over 18 years of age applying for an SSN for the first time must attend in person and provide appropriate identification.)

A child born abroad to a U.S. citizen qualifies for United States citizenship even if the child is a resident of a foreign country and if the other parent is not a U.S. citizen. An SSN is required for all children born before December 1996.

ITINs are for federal tax reporting only and are not intended to serve any other purpose. IRS issues ITINs to help individuals comply with the U.S. tax laws and to provide a means to efficiently process and account for tax returns and payments for those not eligible for Social Security Numbers (SSNs).

An ITIN does not authorize work in the U.S. or provide eligibility for Social Security benefits or the Earned Income Tax Credit.

IRS issues ITINs to foreign nationals and others who have federal tax reporting or filing requirements and do not qualify for SSNs. A non-resident alien individual not eligible for an SSN who is required to file a U.S. tax return only to claim a refund of tax under the provisions of a U.S. tax treaty needs an ITIN.

Other examples of individuals who need ITINs include:

Aliens who are required to have an individual taxpayer identification number (ITIN), but are not eligible to obtain a Social Security number, must file Form W-7, Application for IRS Individual Taxpayer Identification Number.

Taxpayers who are applying for an ITIN to file a tax return must attach original or certified copies, completed return to Form W-7 to get the ITIN. After Form W-7 has been processed, the IRS will assign an ITIN to the return and process the return as if it were filed at the address listed in the tax return instructions.

You may also apply using the services of an IRS-authorized Acceptance Agent or visit some key IRS Taxpayer Assistance Center in lieu of mailing your information to the IRS in Austin. Taxpayer Assistance Centers (TACs) in the United States provide in-person help with ITIN applications on a walk-in or appointment basis.

The information below highlights improvements to the ITIN program. They go into effect on January 1, 2013.

“If you are applying directly to the IRS for an ITIN, we will only accept original identification documents or certified copies of these documents from the issuing agency along with a completed Form W-7 and Federal tax return”.

In order to file your application, you will need to prove your claims of alien status and identity. The following copies of documents certified by the issuer are required for this purpose:

1) Passport or INS document establishing the non-U.S. status and residence of the applicant; or

2 )Foreign birth record and one of the following, which must bear a photograph, has not expired, and is not older than three years:

3) If the applicant is residing in the United States, please provide the U.S. visa or other proof of ineligibility for an SSN.

Allow 6 weeks for the IRS to notify you of your new ITIN on Form 9844 (8 to 10 weeks if you submit documents. If you have not received your ITIN or correspondence at the end of that time, you can call the IRS to find out the status of your application.

Have you withdrawn a portion of your retirement funds early because of the pandemic and are now stuck with paying the 10% early withdrawal penalty? Many people have found themselves in financial hardship and have needed to take out some of their retirement funds before the mandated retirement age. Normally, early distributions made prior to turning 59.5 years of age have been subject to penalties and income tax. However, in light of the pandemic, the IRS has recently released some guidance regarding early withdrawals.

In the recent publishing of IRS Notice 2020-50, the IRS addressed coronavirus-related distributions within the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Here is the basic rundown of the benefits:

|

To qualify for assistance, the IRS requires an ‘acceptable self-certification’:

|

|

Learn how we turned Martha’s $22,000 tax liability into a tax refund:

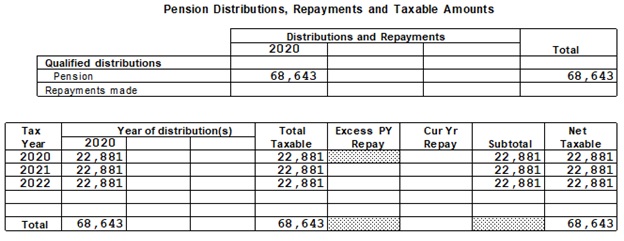

Martha came to us after she withdrew $68,643 from her pension plan. Since she distributed her funds before the mandated retirement age, she accrued $6,864 in penalties. On top of the penalties, there are also federal and state taxes, adding $16,000 to her overall bill. Before Martha came to us, she owed $22,864 in taxes and penalties.

Her husband's furlough from his job last August qualified the couple for relief. After consulting Alejandro, our EA and tax advisor, she was able to abate the $6,864 penalty entirely and split her withdrawal into three separate, taxable distributions. For the years 2020, 2021, and 2022, she will recognize $22,881 from her retirement plan. This way, Martha can meet her family's needs while paying only a fraction of what she owed in taxes. In the end, reducing her taxable income resulted in Martha receiving a tax refund for the 2020 tax year. Thanks to Alejandro, Martha went from being tens of thousands of dollars in debt to the IRS to have the IRS owe her money back during a time of need.

If Martha's story sounds familiar to you, don't let this opportunity pass by. Schedule an appointment at Mendoza&Co today to see how we can work for your tax needs.

Download a copy of the Taxpayer Bill of Rights (en español.)

Mendoza & Company, Inc. is a full-service accounting, Payroll, and Tax Resolution firm in Bethesda, MD and Miami, FL. As a client, you gain a professional team with expertise in multiple fields, providing you the right advice to strengthens your organization and long-term goals.