Blog - Tax Related

Effectively Connected Income (ECI)

TAXATION OF FOREIGN REAL ESTATE INVESTORS IN THE U.S.

30% FLAT TAX ON RENTAL PROPERTY

The article was prepared for educational purposes only. The article is neither legal nor tax advice, nor is it to be construed as such. Each individual’s circumstances are different; you should seek legal and/or tax advice to address any specific question you may have.

RENTAL INCOME: FDAP

U.S. “Fixed, Determinable, Annual or Periodic” (FDAP) Income Tax for Nonresident Alien

Under U.S. Title 26, IRS section code § 871(a)(1), FDAP income includes rental real estate income received on rental property as passive income. FDAP rental income is taxed at a flat tax rate of 30% of the “Gross Rental Income” for the calendar year. The tax applies to foreign persons earning rental income in the U.S. or the lower tax rates under a tax treaty between the investor’s country of residence and the U.S.

In a tax examination, the IRS determines taxable income (FDAP income) as the total rental income collected during the taxable year. All expenses are foregone and non-deductible. No deductions for management fees, property taxes, mortgage interest expenses, depreciation, repairs and maintenance, and other rental costs on the IRS Form Schedule-E “Supplemental Income and Loss” are allowed. FDAP disallows all rental deductions unless the Effectively Connected Income (ECI) is filed.

Example: Mathis and Carol Dubois are Argentinian citizens living in Argentina, and in December 2016, they purchased a rental property at Pike & Rose in North Bethesda. In 2017, the couple contracted a local rental management company to rent out a two-bedroom condo with two baths and a living space of 1,291 square feet for $3,000.00 monthly, a bargain in the area.

The property was rented in 2017 for the entire year. The total annual rental gross income was $36,000.00, and it had $37,257 in qualified rental expenses. The rental LOSS was ($1,257), and the couple’s nontaxable cash-flow for the year was $10,970.00. The benefit of rental property is the deprecation deduction allowed for rental real estate. For the Dubois, the rental property depreciation for 2017 was $12,197.00, and the same amount is to be deducted for the next 27.5 years. During the period, the Dubois nontaxable cash-flow is estimated to be $301,675.00. Not a bad deal for investing in the U.S.

Without knowing about the tax implications of FDAP, the couple engages a local tax preparer to help file the 2017 Form 1040NR “U.S. Nonresident Alien Income Tax Return” and reports the ($1,257) loss on their Schedule-E.

The Dubois are excited with the zero tax liability for the next 27.5 years and consider buying a second investment property in October 2019. In May 2019, the couple calls their friend Rachel, a Maryland licensed real estate agent, about making an investment in a new property. Rachel was involved in the previous acquisition, and the Dubois regard her as the couple's real estate guru.

Rachel is excited about getting a call from the Dubois and equally enthusiastic that her international investor ledger is growing. The plan is set for October 2019, and Rachel puts on her real estate guru hat and searches properties for the Dubois to evaluate. The Dubois’ investment goals are as follows; two bedrooms, two baths, 1,300 square feet, Fair Market Value of $700,000, with a $140,000 down payment plus closing cost.

In September 2019, The IRS audited the Dubois’ 2017 tax return and disallowed the $37,257 rental expenses under the FDAP regulations. The IRS assesses a tax liability of $10,800.00 plus a 75% civil fraud penalty (Section 6663(a)), plus failure to deposit penalty, plus failure to pay penalty and interest. Total tax assessment for 2017 is $20,000+. Further, $10,800 is the yearly estimated tax for each year the property is rented. According to this annual number, the couple will pay an estimated $297,000 in taxes for the next 27.5 years under FDAP ($10,800.00 x 27.5 years).

The new investment property deal is off the table after the bad news from the IRS. Rachel is fired on the spot, and she is blamed for not providing them with tax advice. Rachel is not responsible for the tax problems, but in the real world, real estate agents are to blame for all matters. Rachel loses the Dubois and the opportunity to grow her international ledger.

All this could have been prevented if Rachel and the Dubois knew about the Effectively Connected Income (ECI) tax incentive, which allows Nonresident Alien Investors to file an IRS tax election in order to be taxed at the “NET BASIS” or the ($1,257) loss in the Dubois’ case. The tax election could have allowed the zero tax result for Dubois’ just the same as US Citizens and resident aliens.

SOLUTIONS:

A foreign investor will need to contact a real estate tax accountant and amend three years of tax returns before an IRS examination. The “key” is before the IRS examination. The investor will need to amend 2018, 2017, and 2016 Form 1040NR and include the ECI election with each amended tax return. Under IRS 6501 and IRS Internal Revenue Manual IRM-25.6.1.6.4 “Statute of Limitations on Assessment,” the IRS has three years to audit and access additional taxes from the due date of the return, or three years after the date the return was filed, whichever is later.

Real estate agents and management companies may have clients at risk for the FDAP regulations and IRS examination. Inform your clients of the risk of FDAP and give us a call for assistance.

EFFECTIVELY CONNECTED INCOME

RENTAL INCOME: ECI

Under U.S Title 26, IRS 871 (d) “net basis” election, the IRS code allows an Effectively Connected Income (ECI) election “to treat real property income as income connected with United States business. In general, a nonresident alien individual who during the taxable year derives any income - from real property held for the production of income and located in the United States” can deduct qualified rental expenses.

The ECI regulations are good news for foreign investors and real estate agents. In the Dubois’ case, the election would have allowed $37,257 in real estate expenses and zeroed out their tax liability. Rachel would have kept the Dubois as clients and grown her international investor ledger.

To qualify for ECI benefits, the investor must;

- Obtain an ITIN or EIN number from the IRS,

- Under IRS 871(d), treat the rental income as EIC,

- Make annual EIC elections for each year the property is rented on Form 1040NR, and

- Provide the correct W-8 form to the management company.

The Dubois represents the typical foreign investor we represent in our Bethesda office nationwide. As a tax firm, we can provide the following services to foreign investors.

Our services include:

- IRS ITIN or EIN investors numbers,

- File annual “Effectively Connected Income” elections with the IRS,

- Prepare and provide management company an annual signed Form W-8ECI,

- File IRS Form 1040NR annually for investors,

- Report Income and Expenses on Schedule E,

- If applicable, represent investors in the IRS examination, audits and tax resolution matters.

You need the right tax team working with you. Consider us, Mendoza, Silva & Company for all of your tax services. Consult with an enrolled agent, CPA, or Tax Attorney to assist with foreign investors buying rental property in the United States.

Call us for a complimentary evaluation at 301-962-1700. Mendoza, Silva & Company is located in Bethesda, Maryland, and Miami, Florida.

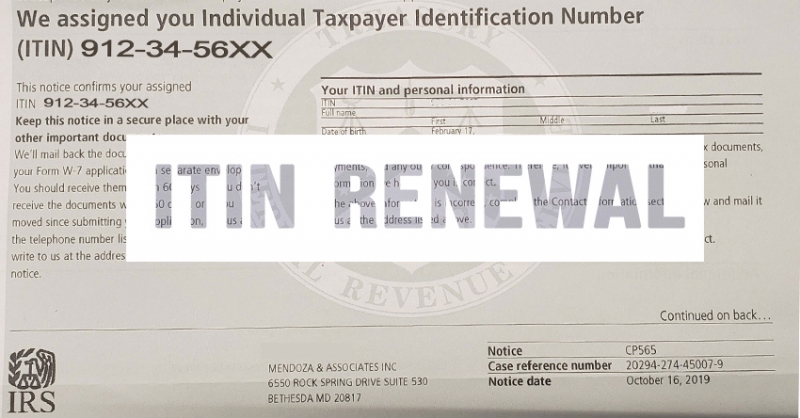

Do You Know When Your ITIN Expired?

The IRS issues Individual Taxpayer Identification Numbers (ITIN) to individuals who are not eligible to obtain a Social Security Number.

Under the Protecting Americans from Tax Hikes (PATH) Act, IRS had established in 2016 tax year the ITIN’s Renewal Program. The rule is simple if an ITIN holder had not filed taxes for the tax years 2016, 2017, or 2018, there ITIN numbers will expire on December 31, 2019. Also, for ITIN’s with middle digits of 83, 84, 85, 86, or 87 (e.g., 9XX-83-XXXX), they will expire at the end of 2019 as well.

Expired ITIN numbers (Middle two digits);

| 2016 | 78 & 79 |

| 2017 | 70, 71, 72 & 80 |

| 2018 | 73, 74, 75, 76, 77, 81 & 82 |

To Expired In 2019 (Middle two digits);

| 2019 | 83, 84, 85, 86 & 87 |

The IRS is sending the Notice “CP-48” to all ITIN holders who must renew their number before December 31, 2019. However, the ITIN holder is not required to wait until receiving this notice to begin the process. If you have an ITIN with middle digits of 83, 84, 85, 86 or 87, you can start the process anytime from now until the end of the year. It is recommended to comply with the renewal as soon as possible to avoid delay from the IRS.

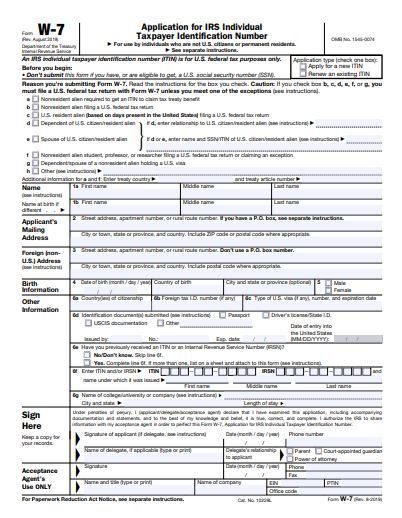

The ITIN renew process is simple, and a tax return is not required to be filed with the request. The taxpayer will need to submit a new Form W7 and supporting documentation to the IRS. However, the IRS does not accept copies of taxpayer supporting documentation unless it is issued by an IRS Agent, Certifying Acceptance Agents (CAA’s).

The Mendoza, Silva & Company team is certified to request your renewal and authenticate your supporting documentation for you. Therefore, you are not at risk of losing your original documents or waiting for weeks until it is returned to you. In our office, we will certify copies of your documents and return your originals to you at the time of your appointment. It is faster and easier!

Avoid common errors now and prevent delays next year

Federal tax returns that are submitted in 2019 with an expired ITIN will be processed. However, certain tax credits and any exemptions will be disallowed. Taxpayers will receive a notice in the mail advising them of the change to their tax return and their need to renew their ITIN. Once the ITIN is renewed, applicable credits and exemptions will be restored and any refunds will be issued.

Additionally, several common errors can slow down and hold some ITIN renewal applications. These mistakes generally center on missing information or insufficient supporting documentation, such as name changes. The IRS urges any applicant to check over their form carefully before sending it to the IRS.

As a reminder, the IRS no longer accepts passports that do not have a date of entry into the U.S. as a stand-alone identification document for dependents from a country other than Canada or Mexico, or dependents of U.S. military personnel overseas. The dependent’s passport must have a date of entry stamp, otherwise the following additional documents to prove U.S. residency are required:

- U.S. medical records for dependents under age 6,

- U.S. school records for dependents under age 18, and

- U.S. school records (if a student), rental statements, bank statements or utility bills listing the applicant’s name and U.S. address, if over age 18.

Link to Acceptance Agents - Maryland

2019 Tax Organizer - Maximize Your Deductions

Download a Tax Organizer Form-Fill-In PDFs for 2019 tax season

These Tax Organizers are designed to help you gather the tax information needed to prepare your personal income or business tax return for 2018. A Tax Organizer is a great tool to help you reduce your taxes or increase your tax refund.

Individuals

2018 Basic Organizer (4 Pages) –This organizer is suitable for clients that are not itemizing their deductions and DO NOT have rental property or self-employment expenses.

2018 Full Organizer (8 Pages) – This organizer includes the information included in the basic organizer, plus entries for itemized deductions, rental properties, and self-employment expenses.

Business

2018 Basic Organizer (4 Pages) – This organizer is suitable for clients with self-employment income, partnership income, and corporation income. (Schedule C, 1065 & 1120s)

We can help you file your tax returns. Schedule Online.

The following are examples of supporting documentation:

- Forms W-2 for wages, salaries, tips, and gambling winnings.

- All Forms 1099 for interest, dividends, retirement, miscellaneous income, social security, state or local refunds, etc.

- Form 1099B Brokerage statements showing investment transactions for stocks, bonds, options, etc.

- Schedule K-1 from partnerships, S-corporations, estates, and trusts.

- Statements supporting educational expenses, deductions or distributions, including any Forms 1098-T, 1098-E, or 1099-Q.

- All Forms 1095-A, 1095-B, and/or 1095-C related to health care coverage for the Premium Tax Credit.

- Statements supporting deductions for mortgage interest, taxes, and charitable contributions, including any Form 1098-Mort.

- Copies of closing statements regarding the sale or purchase of real property.

- Legal papers for adoption, divorce, or separation involving custody of your dependent children.

- Any tax notices sent to you by the IRS or other taxing authority.

- A copy of your income tax return from last year, if not prepared by Mendoza, Silva & Company.

Call us today at 301-962-1700.

Passport Alert – IRS Tax Debts May Revoke Your Passport Featured

Written by Super User

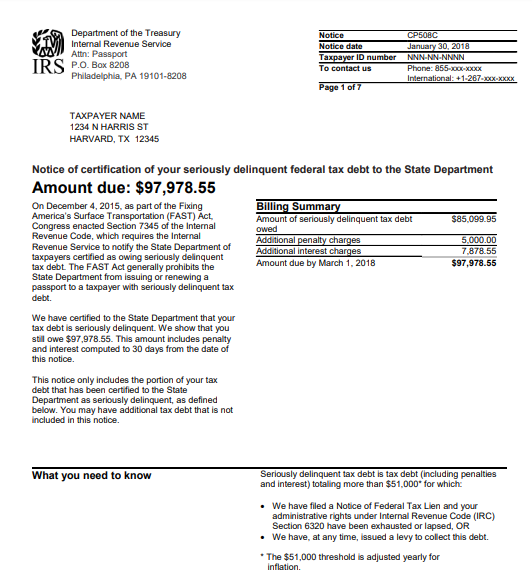

Owing more than $51,000.00 of taxes can stop your travel plans.

Beginning in 2018, The IRS started mailing to Taxpayers owing more than $51,000.00 a notice called "CP508C - Notice of Certification of your Seriously Delinquent federal tax debt to the State Department".

If you owe taxes over $51,000, the IRS may inform the State Department which can then revoke your passport. And you might not even know until you get to the airport.

"On December 4, 2015, as part of the Fixing America’s Surface Transportation (FAST) Act, Congress enacted Section IRC §7345 of the Internal Revenue Code, which requires the Internal Revenue Service to notify the State Department of taxpayers owing more than $51,000.00 and certifying the Taxpayer as “Seriously Delinquent. The FAST Act generally prohibits the State Department from issuing or renewing a passport to a Taxpayer with seriously delinquent tax debt. (per IRS)"

The IRS has the following power if you don’t act soon;

- Filed a Notice of Federal Tax Lien,

- Issued a levy to collect the debt to your employer or from your customers,

- If you apply for a passport or passport renewal, the State Department will deny your application,

- If you currently have a valid passport, the State Department may revoke your passport or limit your ability to travel outside the United States.

It is estimated that about 270,000 Taxpayers are about to receive Notice CP508C in 2019.

Step 1: What to Do?

- Give us a call,

- Request the IRS to provide the detail of accounting for the years and the balances under question. We will call on your behalf and request IRS “Account Transcripts.”

- Evaluate the Account Transcripts for missing payments and locate the canceled check(s) for account adjustments.

- Verify if the amount owed is correct.

Step 2: Propose a Viable Collection Alternative

- Stablish Installment agreement (IA). The installment agreement must be accepted with the IRS prior the passport revocation can be reversed.

- Offer in Compromise (OIC). Same as IA, it must be accepted.

- Request for an Innocent Spouse Relief. While the request is pending, reversal is available. IRC §6015(e)(1)(B) prohibits enforcement while the application is pending. If the debt is related to your spouse income or business and you did not participate in the business activity, Innocent Spouse Relief can be a good avenue for passport revocation reversal. The key is that the request does not need to be accepted by the service. It only needs to be pending.

Key Facts

Before denying a passport, the State Department will hold the application for 90 days to allow a citizen to:

Before denying a passport, the State Department will hold the application for 90 days to allow a citizen to:

- Resolve any erroneous assessment issues (Incorrect tax debts or identity theft matters)

- Make full payment of their debt,

- Enter into a satisfactory payment arrangement – IRM 5.1.12.27.7(6).

Reversal Certification under IRC §7345(c)

You have established a collection alternative with the IRS and accepted. The IRS must give notice to the State Department reversing the certification if:

- Certification is found to be erroneous,

- Debt is legally unenforceable,

- Debt is fully satisfied,

- Debt is no longer “seriously delinquent” per §7345(b),

- Installment Agreement is entered into,

- Offer in Compromise is accepted,

- Justice Department enters into a settlement agreement,

- Innocent Spouse Relief is requested.

Once the (IA) and (OIC) are accepted or Innocent Spouse Relief request is pending, the IRS will mail the “Reversal” notice to taxpayer CP508R and to the State Department.

If you have questions or concerns about the passport revocation, please call Mendoza, Silva & Company today!

We are here to help.

2018 Child & Dependent Tax Credits

Increased to $2,000 in 2018

The child tax credit increases in 2018 to $2,000 (up from $1,000) with up to $1,400 being refundable. The earned income threshold is reduced to $2,500 (down from $3,000 in 2017) allowing more taxpayers to qualify for the credit. A child has to be under the age of 17 and have a valid Social Security number issued before the return due date to qualify for the credit.

In addition, a non-refundable tax credit of $500 is available for each non-child dependent that does not qualify for the child tax credit. The AGI thresholds at which the credit begins to phase out are substantially increased: to $400,000 for married filing jointly and $200,000 for all other taxpayers.

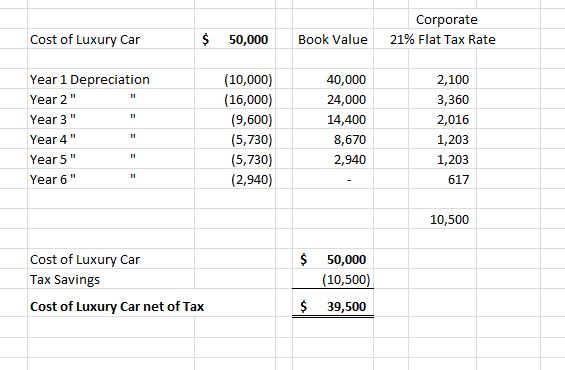

2018 Luxury Auto Limits for Business Auto Deductions

Luxury Auto Limits for Business Autos

The 2018 tax bill increased the luxury auto depreciation deduction limits for the 1st, 2nd, 3rd and subsequent years with the year first increased to $10,000 and the second year to $16,000.

What is a Luxury Auto?

The IRS definition of a "luxury vehicle," is a four-wheeled vehicle regardless the cost of the vehicle, used mostly on public roads, and has an unloaded gross weight of no more than 6,000 pounds.

What is the Corporate Tax Savings?

The most dramatic changes made by the 2018 Tax bill is on the corporate rate. For starters, the bill lowers the corporate tax rate to a flat 21% on all profits from 35% through January 1, 2026. This is not only a massive tax-cut, but is a major simplification as compared to the 2017 corporate tax rates. The flat 21% corporate tax change can save an entity up to $10,500.00 in corporate taxes for an auto costing $50,000.

Here is an example of a Luxury Auto costing $50,000 and put in services on January 1, 2018. Notice, the tax saving is $10,500 over five and half years and resulting in the actual cost to $39,500 net of corporate taxes.

If you have questions about your Luxury Auto tax saving for a corporation, please give this office a call at 301-962-1700.

H.R.1 - An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for the fiscal year 2018.

How to Save for a Child's College Education

Article Highlights:

- Planning for a Child’s College Education

- Tax-Favored Plans

- Tax-Free Earnings

- Coverdell Accounts

- Qualified Tuition Plans

- Have Others Contribute

- Gift Tax Issues

A frequently asked question is, “How might I save for a child’s college education?” The answer depends on how much education is expected to cost and how much time is left until the child heads off to college or university.

The amount of funds that will be required will depend upon whether your child will be attending a local college, attending a local college and then transferring to a university, or going straight to the university. If attending college locally, you generally only need to be concerned about tuition, and the child can live at home, whereas attending a university unless it is local, will add the cost of housing and food on top of substantially higher university tuition. Another factor is whether the student will leave school after obtaining a bachelor’s degree or will be doing graduate studies for an advanced degree.

When the time comes, your child may qualify for a scholarship or grant, but you can’t depend on that when working out a college savings plan.

The federal tax code has two beneficial savings plans that can be used. In both plans, there is no tax benefit to making any contributions. The benefit is that growth due to appreciation in investments if any, and earnings (dividends and interest) are tax-free when withdrawn for qualified education expenses. Thus, the sooner the plan is started, the better because it will have more years to grow in value.

More tax benefit is gained by front-loading the contributions and thus having a larger amount on which to compound the growth and earnings. You should also be aware that anyone, not just you, can make a contribution to the child’s college savings plans. So if your child has any well-heeled grandparents, other relatives or friends who would like to help, they can also contribute.

The two savings plans currently available for college savings are the Coverdell Education Savings Account and the Qualified Tuition Plan, most commonly referred to as a Sec. 529 Plan (529 denotes the section of the tax law code that governs it).

Coverdell Education Savings Account – This plan only allows up to $2,000 in contributions per year, and although it allows withdraws for kindergarten education and above, the contribution limitations generally rule it out as a practical method for college savings.

Sec 529 Plan – This approach is likely your best option. State-run Sec. 529 plan benefits are limited to postsecondary education, but they allow significantly larger amounts to be contributed; multiple people can each contribute up to the gift tax limit each year without being subjected to gift tax reporting. This limit is $15,000 for 2018. A special rule allows contributors to make up to five years of contributions in advance (for a total of $75,000 in 2018).

Sec. 529 plans allow taxpayers to put away larger amounts of money, limited only by the contributor’s gift tax concerns and the contribution limits of the intended plan. There are no limits on the number of contributors, and there are no income or age limitations. The maximum amount that can be contributed per beneficiary (the intended student) is based on the projected cost of college education and will vary between the states’ plans. Some states base their maximum on an in-state four-year education, but others use the cost of the most expensive schools in the U.S., including graduate studies. Most have limits in excess of $200,000, with some topping $370,000. Generally, additional contributions cannot be made once an account reaches that level, but that doesn’t prevent the account from continuing to grow.

When the time comes for college, the distributions will be part earnings/growth in value and part contributions. The contribution part is never taxable, and the earnings part is tax-free if used to pay for qualified college expenses. In addition, the portion of the distribution that represents the return on the contributions and is used for qualified education expenses qualifies for the American Opportunity Tax Credit, which can be as much as $2,500, provided your income level does not phase it out.

For additional details or assistance in planning for a child’s higher education, please give this office a call.

Using Online Agents to Rent Your Home Short Term?

You May Be Surprised at the Tax Ramifications

Article Highlights:

- Schedule C vs. Schedule E

- Rentals of Less Than15 Days

- Rentals of 7 Days or Less

- Rentals of 8 to 30 Days

- An exception to the 30-Day Rule

If you are among the many taxpayers renting your first or second home using rental agents or online rental services that match property owners with prospective renters, such as Airbnb, VRBO and HomeAway, then you should know the IRS has special rules related to short-term rentals.

When property is rented for short periods, special (and sometimes complex) taxation rules come into play, which can make the rents excludable from taxation; other situations may force the rental income and expenses to be reported on Schedule C (as opposed to Schedule E). If you have been renting your home or second home for short periods of time, here is a synopsis of the rules governing short-term rentals so you can prepare yourself for the upcoming tax season.

- Rented for Fewer Than 15 Days During the Year: If you rent your property for fewer than 15 days during the tax year, the rental income is not reportable, and the expenses associated with that rental are not deductible. However, interest and property taxes are still deductible as itemized deductions on your Schedule A.

- Rented for an Average of 7 Days or Less: Under normal circumstances, rentals are treated as passive activities, which are reported on a Schedule E, and net profit from the rental activity is not subject to self-employment tax. But the special rules treat short-term rentals averaging 7 days or less as a trade or business similar to that of a hotel or motel, with the income and expenses reported on Schedule C, and the profits are subject to both income tax and self-employment tax.

- Rented for an Average of 8 to 30 Days: Even rentals for longer than 7 days are treated as a trade or business when substantial personal services are provided to the short-term tenant. Substantial services are those that are primarily for your tenant's convenience, such as regular cleaning, changing linen, or maid service. Substantial services do not include the furnishing of heat and light, the cleaning of public areas, trash collection, and such.

When extraordinary services are provided, the rental is treated as a trade or business and reported on Schedule C regardless of the average rental period. However, it would be extremely rare for this to apply to short-term rentals of your home or second home.

- Exception to the Significant Services Rule – If the personal services provided are similar to those that generally are provided in connection with long-term rentals of high-grade commercial or residential real property (such as the cleaning of public areas and trash collection), and if the rental also includes maid and linen services at a cost of less than 10% of the rental fee, then the personal services are neither significant nor extraordinary for the purposes of the 30-day rule.

A loss from this type of activity, even when reported on your Schedule C as a trade or business, is still treated as a passive activity loss and can only be deducted against passive income. The $25,000 loss allowance that applies to some Schedule E rentals is not available for rental activities reportable on Schedule C.

It is important that you keep a record of not only the rental income from each tenant but also the duration of each rental, so the average rental term for the year can be determined. If you have questions about your rental activities, please give this office a call.

Tax Time Has Arrived! Are You Ready?

Article Highlights:

|

|

If you're like most taxpayers, you find yourself with an ominous stack of "homework" around TAX TIME! Pulling together the records for your tax appointment is never easy, but the effort usually pays off in the extra tax you save! When you arrive at your appointment fully prepared, you'll have more time to:

|

|

Choosing Your Best Alternatives - The tax law allows a variety of methods of handling income and deductions on your return. Choices you make as you prepare your return often affect not only the current year but future returns as well. Topics these choices relate to including:

- Sales of property - If you're receiving payments on a sales contract over a period of years, you can sometimes choose between reporting the whole gain in the year you sell or over a period of time as you receive payments from the buyer.

- Depreciation - You're able to deduct the cost of your investment in certain business properties. You can either depreciate the costs over a number of years; or, in certain cases, deduct them all in one year.

Where to Begin? Preparation for your tax appointment should begin in January. Right after the New Year, set up a safe storage location, such as a file drawer, cupboard, or safe. As you receive pertinent records, file them right away, before you forget or lose them. Make this a habit, and you'll find your job a lot easier on your appointment date. Other general suggestions to prepare for your appointment include:

- Segregate your records according to income and expense categories. File medical expense receipts in one envelope or folder, mortgage interest payment records in another, charitable donations in a third, etc. If you receive an organizer or questionnaire to complete before your appointment, fill out every section that applies to you. (Important: Read all explanations and follow instructions carefully. By design, organizers remind you of transactions you may otherwise miss.)

- Call attention to any foreign bank account, foreign financial account, or foreign trust in which you have an ownership interest, signature authority, or controlling stake. We also need to know about foreign inheritances and ownership of foreign assets. In short, bring any foreign financial dealings to our attention so we know if you have any special reporting requirements. The penalties for not making and submitting required reports can be severe.

- If you acquired your health insurance through a government Marketplace you will receive Form 1095-A, issued by the Marketplace that will include information needed to complete your return. In addition, you will need to provide proof of insurance to avoid a penalty or qualify for one of the many exemptions from the penalty. If you received a hardship penalty exemption from the Marketplace you will have been issued an exemption certificate number (ECN). That number must be included on your tax return. The 1095-A and ECN documentation need to be included with the other material you bring to your appointment. If your insurance coverage was through an employer, and the employer issued Form 1095-B, 1095-C or a substitute form detailing your coverage, bring it to the appointment.

- Keep your annual income statements separate from your other documents (e.g., W-2s from employers, 1099s from banks, stockbrokers, etc., and K-1s from partnerships). Be sure to take these documents to your appointment, including the instructions for K-1s!

- Write down questions so you don't forget to ask them at the appointment. Review last year's return. Compare your income on that return to your income in the current year. A dividend from ABC stock on your prior-year return may remind you that you sold ABC this year and need to report the sale, or that you haven't yet received the current year's 1099-DIV form.

- Make sure you have social security numbers for all your dependents. The IRS checks these carefully and can deny deductions and credits for returns filed without them.

- Compare deductions from last year with your records for this year. Did you forget anything?

- Collect any other documents and financial papers that you're puzzled about. Prepare to bring these to your appointment so you can ask about them.

Accuracy Even for Details - To ensure the greatest accuracy possible in all detail on your return, make sure you review personal data. Check name(s), address(es), social security number(s) and occupation(s) on last year's return. Note any changes for this year. Although your telephone numbers and e-mail address aren't required on your return, they are always helpful should questions occur during return preparation.

Marital Status Change - If your marital status changed during the year, if you lived apart from your spouse or if your spouse died during the year, list dates and details. Bring copies of prenuptial, legal separation, divorce or property settlement agreements, if any, to your appointment. If your spouse passed away during the year, you should have a copy of his or her trust agreement or will available for review.

Dependents - If you have qualifying dependents, you will need to provide the following for each (if you previously provided us with items 1 through 3 you will not need to supply them again):

|

|

For anyone other than your child to qualify as your dependent, they must pass five strict dependency tests. If you think one or more other individuals qualify as your dependents (but you aren't sure), tally the amounts you provided toward their support vs. the amounts they provided. This will simplify the final decision.

Some Transactions Deserve Special Treatment - Certain transactions require special treatment on your tax return. It's a good idea to invest a little extra preparation effort when you have had the following transactions:

- Sales of Stock or Other Property: All sales of stocks, bonds, securities, real estate and any other property need to be reported on your return, even if you had no profit or loss. List each sale, and have purchased and sale documents available for each transaction.

The purchase date, sale date, cost, and selling price must all be noted on your return. Make sure this information is contained in the documents you bring to your appointment. - Gifted or Inherited Property: If you sell the property that was given to you, you need to determine when and for how much the original owner purchased it. If you sell the property you inherited, you need to know the original owner's death-date and the property's value at that time. You may be able to find this on estate tax returns or in probate documents; otherwise, ask the executor.

- Reinvested Dividends: You may have sold stock or a mutual fund in which you participated in a dividend reinvestment program. If so, you will need to have records of each stock purchase made with the reinvested dividends.

- Sale of Home: The tax law provides special breaks for home sale gains, and you may be able to exclude up to $500,000 of the gain from your primary home if you file a married joint return and meet certain ownership, occupancy, and holding period requirements. The maximum exclusion is $250,000 for others. Since the cost of improvements made in your home can also be used to reduce any gain, it is good practice to keep a record of them. The exclusion of gain applies only to a primary residence; so keeping a record of improvement to other property, such as your second home, is important. Be sure to bring a copy of the sale documents (usually the closing escrow statement).

- Purchase of a Home: Be sure to bring a copy of the final closing escrow statement if you purchased a home.

- Vehicle Purchase: If you purchased a new plug-in electric car (or cars) this year, you may qualify for special credit. Please bring the purchase statement to the appointment with you.

- Home Energy-Related Expenditures: If you installed a solar-electric system on your home or second home, please bring the details of the purchase and manufacturer's credit qualification certification to your appointment. You may qualify for a substantial energy-related tax credit.

- Identity Theft: Identity theft is rampant and can impact your tax filings. If you have reason to believe that your identity has been stolen, please contact this firm as soon as possible. The IRS provides special procedures for filing if you have had your identity stolen.

- Car Expenses: Where you have used one or more automobiles for business, list the expenses of each separately. The government requires your total mileage, business miles, and commuting miles for each business use of your car to be reported on your return, so be prepared to have those numbers available. If you were reimbursed for mileage through an employer, know the reimbursement amount and whether it is included in your W-2.

- Charitable Donations: You must substantiate cash contributions (regardless of amount) with a bank record or written communication from the charity showing the name of the charitable organization, date and amount.

Unreceipted cash donations put into a "Christmas kettle," church collection plate, etc., are not deductible. For clothing and household contributions, items donated must generally be in good or better condition, and items such as undergarments and socks are not deductible. You must keep a record of each item contributed that indicates the name and address of the charity, date, and location of the contribution, and a reasonable description of the property. Contributions valued under $250 and dropped at an unattended location do not require a receipt. For contributions above $500, the record must also include when and how the property was acquired and your cost basis in the property. For contributions above $5,000 and other types of contributions, please call this office for additional requirements.

If you have questions about assembling your tax data prior to your appointment, please give this office a call.

How Small Businesses Write Off Equipment Purchases

Article Highlights:

|

|

From time to time, the owner of a small business will purchase equipment, office furnishings, vehicles, computer systems, and other items for use in the business. How to deduct the cost for tax purposes is not always an easy decision because there are a number of options available, and the decision will depend upon whether a big deduction is needed for the acquisition year or more benefit can be obtained by deducting the expense over a number of years using depreciation. The following are the write-off options currently available.

- Depreciation – Depreciation is the normal accounting way of writing off business capital purchases by spreading the deduction of the cost over several years. The IRS regulations specify the number of years for the write-off based on established asset categories, and generally for small business purchases the categories include 3-, 5- or 7-year write-offs. The 5-year category includes autos, small trucks, computers, copiers, and certain technological and research equipment, while the 7-year category includes office fixtures, furniture, and equipment.

- Material & Supply Expensing – IRS regulations allow certain materials and supplies that cost $200 or less, or that have a useful life of less than one year, to be expensed (deducted fully in one year) rather than depreciated.

- De Minimis Safe Harbor Expensing – IRS regulations also allow small businesses to expense up to $2,500 of equipment purchases. The limit applies per item or per invoice, providing a substantial leeway in expensing purchases. The $2,500 limit is increased to $5,000 for businesses that have an applicable financial statement, generally large businesses.

- Routine Maintenance – IRS regulations allow a deduction for expenditures used to keep a unit of property in the operating condition where the business expects to perform the maintenance twice during the class life of the property. Class life is different than a depreciable life.

Depreciable Item Class Life Depreciable Life Office Furnishings 10 7 Information Systems 6 5 Computers 6 5 Autos & Taxis 3 5 Light Trucks 4 5 Heavy Trucks 6 5 - Unlimited Expensing – The Tax Cuts and Jobs Act passed in December 2017 includes a provision allowing 100% unlimited expensing of tangible business assets (except structures) acquired after September 27, 2017, and through 2022. Applies when a taxpayer first uses the asset (can be new or used property).

- Bonus Depreciation – The tax code provides for a first-year bonus depreciation that allows a business to deduct 50% of the cost of the newest tangible property if it is placed in service during 2017. The remaining cost is deducted over the asset's depreciable life. The 50% rate applies for new property placed in service prior to September 28, 2017, and, by-election, to new or used property, acquired and first put into use by the taxpayer after September 27, 2017, and before December 31, 2017.

- Sec 179 Expensing – Another option provided by the tax code is an expensing provision for small businesses that allows a certain amount of the cost of tangible equipment purchases to be expensed in the year the property is first placed into business service. This tax provision is commonly referred to as Sec. 179 expensing, named after the tax code section that sanctions it. The expensing is limited to an annual inflation-adjusted amount, which is $510,000 for 2017 and $1 million for 2018. To ensure that this provision is limited to small businesses, whenever a business has purchases of property eligible for Sec 179 treatment that exceeds the year's investment limit ($2,030,000 for 2017 and $2.5 million for 2018), the annual expensing allowance is reduced by one dollar for each dollar the investment limit is exceeded.

An undesirable consequence of using Sec. 179 expensing occurs when the item is disposed of before the end of its normal depreciable life. In that case, the difference between normal depreciation and the Sec. 179 deduction is recaptured and added to income in the year of disposition. - Mixing Methods – A mixture of Sec. 179 expensing, bonus depreciation and regular depreciation can be used on a specific item, allowing just about any amount of write-off for the year for that asset.

For some individual taxpayers, the alternative minimum tax (AMT) may be a concern. Bonus depreciation and Sec. 179 expensing are not preference items, and therefore their use will not trigger an AMT add-on tax. However, the difference between 200% MACRS depreciation, if claimed, and 150% MACRS depreciation is a preference item for AMT and could cause or add to the AMT tax

More...

Maximize Your Tax Refunds with Our Checklist and Organizers

Tax Season is Here. We can help you with your tax preparation. Call us and schedule an appointment today! .....

Open Monday through Friday 9-7pm and Saturdays from 9-6pm. Our professionals are licensed and in good standing with Maryland Department of Licenses and Regulations.

You will need the following personal information to do your taxes;

|

|

Tax Documents for the current year;

|

|

Before you begin to organize your documents download the attached organizers to help you maximize your refund.

New Tax Changes on Home Mortgage Interest

Tags: Home and Mortgage, Tax Planning

Article Highlights:

|

|

Note: The is one of a series of articles explaining how the various tax changes made by the GOP's Tax Cuts & Jobs Act (referred to as the "Act" in the article), passed late in December 2017, might affect you and your family in 2018 and future years, and offering strategies you might employ to reduce your tax liability under the new tax laws.

For years, taxpayers have been able to deduct home mortgage interest on their primary and second homes as an itemized deduction, subject to certain limitations. The interest deduction was limited to the interest on up to $1 million of acquisition debt and $100,000 of equity debt.

Acquisition debt is the debt incurred to purchase, construct or substantially improve a taxpayer's principal or second home. So when you purchased your home, that original loan was acquisition debt, and if you later borrowed additional money that you used to add a room, pool, etc., that loan was also acquisition debt. However, if the total of all of your acquisition loans exceeded the $1 million limit, then the interest on the excess debt over $1 million was not deductible as acquisition debt interest.

Consumer debt interest, such as interest on auto loans and credit card debt, is not deductible as an itemized deduction. However, years ago, Congress allowed homeowners to deduct the interest on up to $100,000 of equity debt. This allowed homeowners to use the equity in their homes for any purpose and deduct the interest on the equity debt as an itemized deduction.

Well, That Has All Changed. For 2018 through 2025, the new tax law reduces the $1 million limit on home acquisition debt to $750,000 ($375,000 for married separate filers), except that the lower limit won't apply to indebtedness incurred before December 15, 2017. That is, the $1M cap continues to apply to acquisition mortgages on primary and second residences that were already in existence prior to December 15, 2017, as well as for taxpayers who entered into a binding written contract before that date to close on the purchase of a principal residence before January 1, 2018, and who purchase that residence before April 1, 2018.

The Equity Debt Interest Deduction Is No More – Congress has yanked the rug out from under those with equity debt on their homes. Beginning in 2018, interest paid on equity debt will no longer be allowed as a deduction, regardless of when the debt was incurred.

This seems a little unfair and can have an adverse impact on individuals who used their home as a piggy bank for personal expense purposes.

Whether any of this makes any difference in light of the new higher standard deduction amounts for 2018, and whether you should be looking for ways to pay down the equity debt, will depend upon the amounts of your other itemized deductions. Please call this office if you have any questions.

Will Your 2018 Withholding Be Right?

Article Highlights:

|

|

Note: The is one of a series of articles explaining how the various tax changes made by the GOP's Tax Cuts & Jobs Act (referred to as the "Act" in the article), passed late in December 2017, might affect you and your family in 2018 and future years, and offering strategies you might employ to reduce your tax liability under the new tax laws.

One of the first trouble spots of the new tax reform is the W-2 withholding for 2018. Passage of the new law in late December hasn't given the IRS much time to develop new withholding tables. This can be a big issue, as the recent Tax Cuts & Jobs Act (TCJA) substantially altered the tax rates and standard deductions, did away with exemption deductions, and increased the child tax credits—all elements of how the withholding allowances and tables have been structured in the past.

On January 11, the IRS released modified withholding tables for employers to use for determining employee withholding. Supposedly the new withholding tables have been crafted to use the information employers already have from employees' prior Form W-4s on file to adjust their employees' withholding, taking into account the tax cuts for individuals included in the TCJA.

The IRS is also working on revising the Form W-4 to reflect additional modifications in the new law, such as changes in available itemized deductions, increases in the child tax credit, the new dependent credit and repeal of the dependent exemptions deduction.

When available, the new Form W-4 can be used by employees who wish to update their withholding in response to the new law or changes in their personal circumstances in 2018 and by workers starting a new job. Until a new Form W-4 is issued, employees and employers should continue to use the 2017 Form W-4.

You are cautioned to keep an eye on your take-home pay to ensure your withholding has not changed too drastically once your employer starts using the new IRS tables. Most wage earners should see a decrease in withholding (and a larger net paycheck), but if the change is too radical you could end up owing tax next year when you file your 2018 return.

If you are self-employed and/or have other sources of taxable income in addition to wages, or if you itemize your deductions, the wage withholding by your employer-based upon your existing Form W-4 probably will not provide the correct withholding, and you may need to make adjustments to your withholding allowances or even make estimated tax payments.

As 2018 is the first year that the vast majority of the provisions of TCJA will apply, you should be cautious that your withholding is not too little, resulting in a tax due next filing season, or too high, denying you the benefits of the tax cut until you receive your refund next year.

Please call this office if you need assistance in determining your withholding or if you have questions about the new tax law.

2018 Standard Mileage Rates Announced

Article Highlights:

As it does every year, the Internal Revenue Service recently announced the inflation-adjusted 2018 optional standard mileage rates used to calculate the deductible costs of operating an automobile for business, charitable or medical purposes.

|

|

Beginning on Jan. 1, 2018, the standard mileage rates for the use of a car (or a van, pickup or panel truck) are:

|

|

The business standard mileage rate is based on an annual study of the fixed and variable costs of operating an automobile. The rate for medical purposes is based on the variable costs as determined by the same study. The rate for using an automobile while performing services for a charitable organization is statutorily set (it can only be changed by Congressional action) and has been 14 cents per mile for over 15 years.

Important Consideration: The 2018 rates are based on 2017 fuel costs. Based on the potential for substantially higher gas prices in 2018, it may be appropriate to consider switching to the actual expense method for 2018, or at least keeping track of the actual expenses, including fuel costs, repairs, maintenance, etc., so that the option is available for 2018.

Taxpayers always have the option of calculating the actual costs of using their vehicle for business rather than using the standard mileage rates. In addition to the potential for higher fuel prices, the extension and expansion of the bonus depreciation as well as increased depreciation limitations for passenger autos in the Tax Cuts and Jobs Act may make using the actual expense method worthwhile during the first year a vehicle is placed in business service. However, the standard mileage rates cannot be used if you have used the actual method (using Sec. 179, bonus depreciation and/or MACRS depreciation) in previous years. This rule is applied on a vehicle-by-vehicle basis. In addition, the business standard mileage rate cannot be used for any vehicle used for hire or for more than four vehicles simultaneously.

Employer Reimbursement – When employers reimburse employees for business-related car expenses using the standard mileage allowance method for each substantiated employment-connected business mile, the reimbursement is tax-free if the employee substantiates to the employer the time, place, mileage and purpose of employment-connected business travel.

The Tax Cuts and Jobs Act eliminated employee business expenses as an itemized deduction, effective for 2018 through 2025. Therefore, employees may no longer take a deduction on their federal returns for unreimbursed employment-related use of their autos, light trucks or vans.

Faster Write-Offs for Heavy Sport Utility Vehicles (SUVs) – Many of today's SUVs weigh more than 6,000 pounds and are therefore not subject to the limit rules on luxury auto depreciation; taxpayers with these vehicles can utilize both the Section 179 expense deduction (up to a maximum of $25,000) and the bonus depreciation (the Section 179 deduction must be applied before the bonus depreciation) to produce a sizable first-year tax deduction. However, the vehicle cannot exceed a gross unloaded vehicle weight of 14,000 pounds. Caution: Business autos are 5-year class life property. If the taxpayer subsequently disposes of the vehicle before the end of the 5-year period, as many do, a portion of the Section 179 expense deduction will be recaptured and must be added back to your income (SE income for self-employed individuals). The future ramifications of deducting all or a significant portion of the vehicle's cost using Section 179 should be considered.

If you have questions related to the best methods of deducting the business use of your vehicle or the documentation required, please give this office a call.

Search

Categories

Recent Posts

-

23 Jan, 202322 Questions About 2022 Taxes

23 Jan, 202322 Questions About 2022 Taxes -

23 Jan, 2023Tax Updates for 2022

23 Jan, 2023Tax Updates for 2022 -

15 Dec, 2021Medical Expense Deductions

15 Dec, 2021Medical Expense Deductions -

-

06 Oct, 2021The IRS Crackdown on Venmo, Zelle Payments

06 Oct, 2021The IRS Crackdown on Venmo, Zelle Payments

About Us

Mendoza & Company, Inc. is a full-service accounting, Payroll, and Tax Resolution firm in Bethesda, MD and Miami, FL. As a client, you gain a professional team with expertise in multiple fields, providing you the right advice to strengthens your organization and long-term goals.